Lender Protection

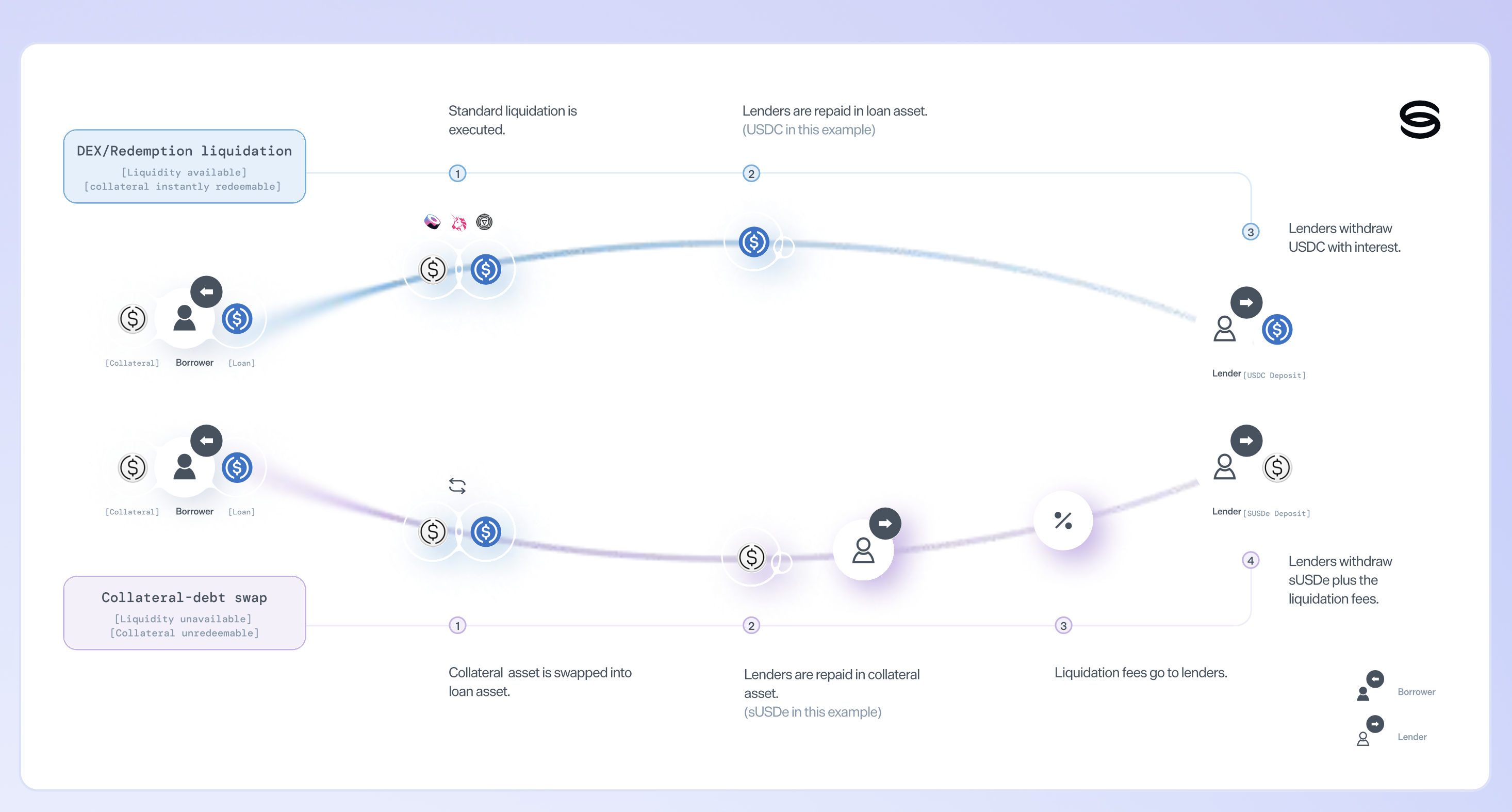

Liquidations ensure that markets remain solvent and lenders can withdraw their funds in full. To protect lenders, Silo supports two types of liquidations:

Collateral-sale liquidations: The market behaves like a traditional lending market where collateral is sold on a DEX to repay the debt.

Internal collateral-debt swap (CDS): The market defaults (erases) outstanding debt and distributes collateral to lenders as reimbursement.

Collateral-sale liquidations

Anyone can perform a liquidation when the collateral value exceeds the configured DEX liquidation threshold (D-LT).

Silo supports partial liquidation. The liquidation module is implemented using the Silo Hooks System and is deployed as a hook.

Liquidations are always permissionless and economically incentivized. After completing a liquidation, the liquidator receives a reward in the form of a liquidation fee. The fee is set per market by the deployer and cannot be changed afterward. Developers can read the fee from the SiloConfig contract.

The Silo liquidation module is designed to support partial liquidations. However, a full liquidation may be executed if the remaining position would leave an uneconomical “dust” balance.

Internal collateral-debt swap (CDS)

The internal collateral-debt swap is a second liquidation engine that can operate alongside the standard collateral-sale liquidation. When the collateral value exceeds the configured CDS liquidation threshold (CDS-LT), instead of selling collateral on a DEX to obtain the borrowed asset, the protocol writes off the borrower’s debt and compensates lenders with the collateral itself at a discount (via collateral share tokens).

Unlike Collateral-Sale, CDS distributes liquidation fees to lenders. This avoids forced onchain swaps during stressed market conditions (e.g., illiquid collateral, shallow liquidity pools, or high price impact).

IMG: Lender's realized liquidation yield

How it works (flow)

The collateral-debt swap mechanism builds on the existing liquidation flow in the Silo Protocol with three key modifications and integrates an Incentive Controller for real-time collateral distribution to lenders.

Step 1 — Liquidation via Share Tokens

During liquidation, the collateral is not sold for the borrowed asset. Instead, collateral share tokens are transferred directly to the Incentive Controller, which immediately distributes them to lenders on the opposite side of the market. This ensures lenders receive the defaulted collateral without requiring any on-chain swaps.

Only share tokens can be used for liquidation under this mode.

Liquidation fee split: If the liquidation fee is set to 20% and the position being liquidated has 1,000 USDC in debt, then 1,200 worth of USDC share tokens are used. This surplus is split between:

-

Lenders (100% of debt + 80% of fee) → receive $1,160 in value via the Incentive Controller

-

Liquidator (20% of fee) → receives $40 in share tokens directly

This split reflects the reduced gas and execution risk in the defaulting model. Liquidators no longer perform swaps or take on price risk, so their incentive can be lower.

Step 2 — Simulated repay

A repay operation is still executed, but without transferring the borrowed asset. Instead, the protocol updates its internal accounting to reflect that the debt has been repaid, even though no borrowed tokens were received. This simulates a repay purely at the accounting level. See repayDebtByDefaulting(...) for the implementation.

Step 3 — Adjusting total collateral assets

Since the borrowed asset (e.g., USDC) is not actually returned to the protocol, the protocol reduces the total collateral assets variable on the borrowed side by the forgiven debt amount. This reflects the lenders’ loss of claim on the original asset and finalizes the write-off.

The insolvent borrower’s position becomes fully cleared — no remaining debt and no further obligations.

Step 4 — Claiming distributed collateral

Lenders must claim their allocated collateral from the Silo Lending App. The claimable amount is distributed pro rata and equals:

-

100% of the forgiven debt plus 80% of the liquidation fee

-

The remaining 20% of the liquidation fee is paid directly to the liquidator.

Summary: Internal collateral-debt swap liquidation

-

Debt write-off with collateral reimbursement: Instead of selling collateral for the borrowed asset, the protocol erases the borrower’s outstanding debt and compensates lenders with collateral share tokens.

-

Share-token-only execution: Liquidation is executed exclusively using collateral share tokens. No underlying collateral is unwrapped and no swaps are performed.

-

Reduced liquidator incentive: Since liquidators do not perform swaps or take price execution risk, the liquidation fee paid to liquidators can be lower than in collateral-sale liquidations.

-

Configurable access control: The internal collateral-debt swap can be configured as either:

-

Permissioned — execution is restricted to approved actors (e.g., keepers, protocol operators, or governance-controlled executors)

-

Parallel operation with standard liquidations: Collateral-sale liquidations and internal collateral-debt swaps can coexist within the same Silo. Liquidators may select the optimal path based on market conditions, with defaulting serving as a fallback mechanism.

-

Higher liquidation threshold (LT): This liquidation path is triggered at a higher LT than collateral-sale liquidations, ensuring it is used as a secondary option when standard liquidations are also enabled.

-

Protocol-level solvency preservation: Lender losses on the borrowed asset are explicitly accounted for by reducing borrowed-side collateral accounting. In return, lenders receive collateral share tokens as compensation via the Incentive Controller.